Making Your First Hard Money Loan--Comping Loan Collateral

Making Your First Hard Money Loan--Comping Loan Collateral

Hard Money Lenders make high-interest-rate (10-14%) loans secured by real estate. Let's break Loan Origination down into 8 steps:

1. Marketing for Borrowers

2. Comping Loan Collateral

3. Loan Structuring & Commitment

4. Collateral File Assembly

5. Title Review

6. Drawing Loan Docs

7. Drawing Lender’s Escrow Instructions

8. Funding & Closing

Previously on Hard Money Monday, I discussed Marketing for Borrowers. Today, I’ll discuss Comping Loan Collateral. For consistency, I’ll focus on single-family fix and flip loans. It's a bread & butter non-owner-occupied investment loan

When comping collateral, your job is to figure out 2 things:

1. the “As Is” house value

2. the After Repaired Value (ARV) of the house

Appraisers have a nuanced system for property condition ratings C1, C2...C6. We ain’t doing that. I divide my world into 3 types of property:

1. Fixers

2. Traditional

3. Renovated

To figure out the as-is value & ARV, you usually want 2-3 fixer comps & 2-3 renovated comps. This doesn’t mean you will get this mix of comps, but its what you are hoping for. Now imagine I airdrop you into a new city and task you with valuing a house for a loan. What do you do? Ideally, you have MLS access and are an agent so you can get inside vacant houses. But let’s assume you don’t and let’s assume you aren’t, as it’s harder.

Today or tomorrow, we’ll be funding a loan on Welton Dr in Albuquerque. It’s a roughly 1900 square foot 3 bedroom 2 bath. The current owner started a renovation but has been unable to finish it. Our borrower is going to spend about $25,000 finishing the renovation.

Here’s how you calculate the as-is value and ARV

Step 1: get on Zillow

Step 2: Look at sales within a mile of the subject property

If there are arterial roads, you likely want comps that are inside the borders of these arterial roads. I will comp the loan collateral to houses +/- 15% in size to it. In this case I’m comping the subject property to 1500-2250 square foot detached single family properties.

What if it's a nondisclosure state (like NM) & you don’t know what comps have sold for?

Talk to the comp's listing & buyers agents

Ask what their comp would sell for today

Ask about the subject property

Agents traffic in information and most are happy to share with private lenders. The upshot to this process is that fat margins live on the other side of opacity. Through conversations with agents, you’ll create a data point mosaic helping you peg the as-is value & ARV of the subject property. Next time you lend there, it will be that much faster and you'll be that much better. Eventually you get to the point that you have an informational edge versus others in the market. For example, you’ll have outstanding loans in the neighborhood that are pending for sale and you’ll be among a handful to know what they’re actually selling for.

I prefer to lend on property that's conforming for its area. Picture a city or neighborhood’s housing inventory inside a bell curve based on the number of beds, baths, garages and size. I want my loan collateral—post business plan—to be in the middle of that bell curve. I’ll let smarter people lend on the tails of the curve. In the middle of a bell curve, I can use that market’s stats (days on market, months of inventory, etc.) as reliable benchmarks for how long it should take to go under contract and sell.

Anything non-conforming (a busy road, near power lines, higher crime rates vs. the comps, flood zone etc), means more work and a likely haircut in both as-is and ARV estimates.

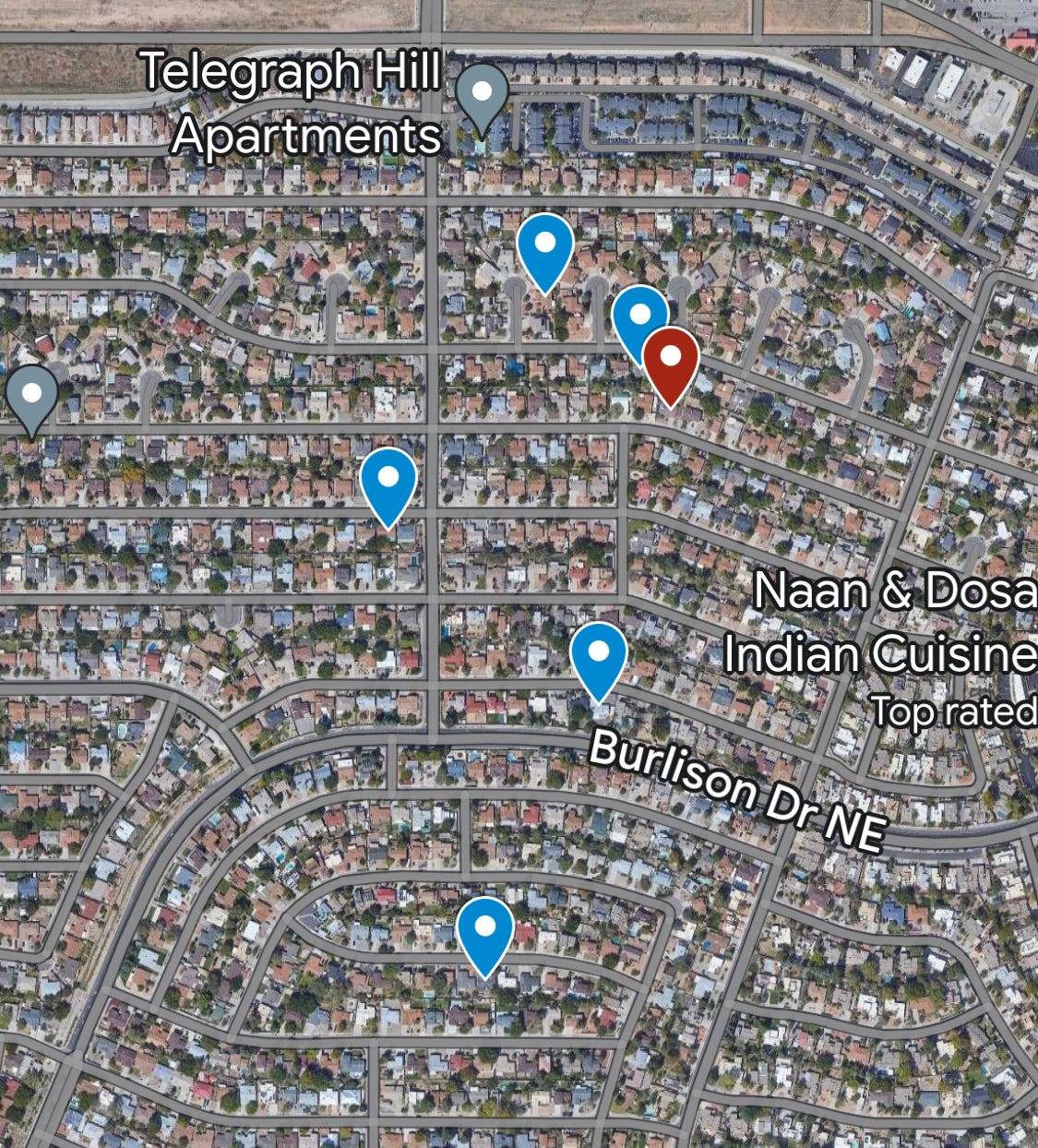

Here’s an image of the comps I used on this loan. The subject loan collateral is in red, while the sold comps are in blue. Note that they’re all within about a half mile of each other and they all closed within the last 6 months.

Comp #1 is 7029 Luella Anne Dr. It is a 3 bedroom 2 bath 1563 square feet and sold for $349,900. It’s what I call a traditional sale, meaning the seller likely lived in the house. The house is kept up but things are dated because homeowners don’t replace everything at once, they replace things over time as budget permits.

Comp #2 is 6920 Avenida La Costa. It is a 3 bedroom 2 bath 1825 square feet and sold for $359,000. It’s what I call a fixer, meaning there’s considerable deferred maintenance. This is an important comp because it puts a floor on the as-is value of the subject property.

Comp #3 is 7108 Marilyn Ave. It is a 3 bedroom 2 bath 1932 square feet and sold for $399K. I don't consider this a great renovation but it's a renovation. The biggest problem with it is you’ve got one color scheme for the finish carpentry and interior paint, and another for the kitchen and flooring. It’s just not a great blend.

Comp #4 is 6900 Hildegarde Dr. It is 4 bedroom 2 bath 1816 square feet and sold for $345,000. I consider this a traditional sale.

The goal is to determine the house’s ARV & create an estimate for how long it will take to sell it once finished. After pulling comps & speaking with brokers here’s where I landed on the collateral value for the Welton Drive loan.

As is Value: $340,000

ARV: $420,000

This opinion of value will inform the next step in the process–Loan Structuring and Commitment. If you are lending in an area that’s unfamiliar, it’s okay to hire an agent knowledgeable about investing to do a broker opinion of value for you. But you can never take their opinion as gospel. In this business it’s critical that you build and exercise your own sense of judgment. In my next edition of Hard Money Monday, I’ll discuss Loan Structuring and Commitment.